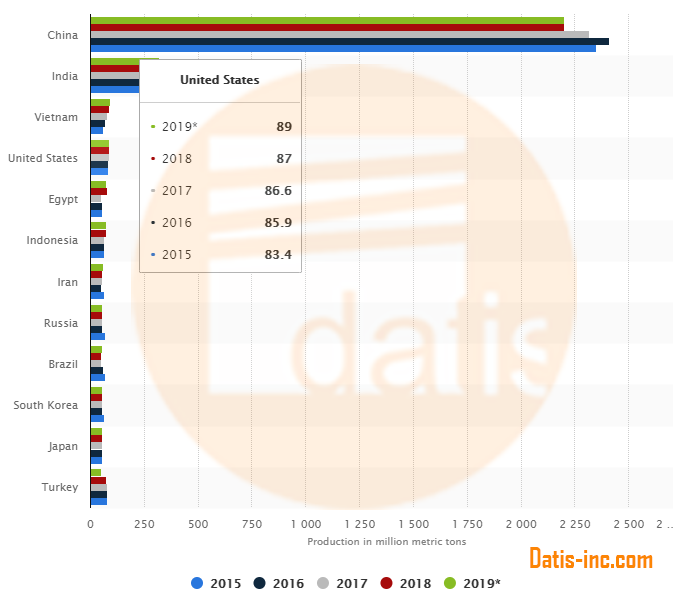

United States

The cement industry in the United States produced 82.8 million tonnes (81,500,000 long tons; 91,300,000 short tons) of cement in 2015, worth US$9.8 billion, and was used to manufacture concrete worth about US$50 billion. The US was the world’s third-largest producer of cement, after China and India (it’s 4th rank now). The US cement industry includes 99 cement mills in 34 states, plus two plants in Puerto Rico. The industry directly employed 10,000 workers in 2015. Ten percent of the cement used in the United States in 2015 was imported.

The types and amounts of cement produced in 2015 were:

- Portland cement 80.4 million tons

- Masonry cement 2.4 million tons

- Other hydraulic cement 0.6 million tons

Cement production is predominantly portland cement, which is mostly used in concrete. Cement for concrete is an essential material for construction, and demand is a function of construction spending. Single-family residential construction is considered only moderately cement-intensive; multifamily residential somewhat more intensive. Nonresidential construction and government construction projects are considered the most cement-intensive.

In 2013, 70.8 percent of portland cement was sold as ready-mix concrete, such as is delivered in cement-mixer trucks. 11.5 percent was sold dry to contractors and construction materials stores; 11.3 percent was sold to manufacturers of concrete products; 4.6 percent was sold for oil and gas wells, and 1.8 percent was sold to government agencies and others.

Because cement is a bulk commodity, transportation can be a significant part of the cost. To minimize transportation costs, cement plants are ideally located close to the market, with access to efficient transportation such as ship or railroad. Most cement plants are located close to the limestone deposits.

Thirty-four states have cement manufacturing plants. In 2013, the five leading cement-producing states, in descending order, were: Texas, California, Missouri, Florida, and Alabama. Together, the five accounted for almost half of US cement production. The list of top five cement-consuming states is similar: Texas, California, Florida, Ohio and Pennsylvania.

In 2015, about 10 percent of US cement consumption came from imports. The largest sources of US cement imports were Canada and Greece.

In 2013, the top producers of portland cement in the US were:

1 – CEMEX

2 – Holcim (now LafargeHolcim)

3 – Lehigh Hanson Inc.

4 – Buzzi Unicem

5 – Ash Grove Cement Company (to be acquired by CRH plc in early 2018)

6 – Lafarge North America (merged with Holcim in 2015)

7 – Texas Industries Inc

8 – Eagle Minerals Inc.

9 – Essroc Cement Corp.

10 – St. Marys Cement Group

In 2013, the top 5 companies produced 54 percent of US portland cement; the top 10 companies produced 78 percent.