President of the People's Republic of Bangladesh

Mr. Mohammad Abdul Hamid is the current President of Bangladesh. He was elected to his first term in April 2013, and re-elected to his current second term in 2018.

Prime Minister of the People's Republic of Bangladesh

Ms. Sheikh Hasina, is a Bangladeshi politician serving as the 10th Prime Minister of Bangladesh, having held the office since January 2009. Having previously served as Prime Minister for five years, she is the longest-serving Prime Minister in the history of Bangladesh.

Shah Cement

10 Million Tonnes per Annum/Cement Capacities

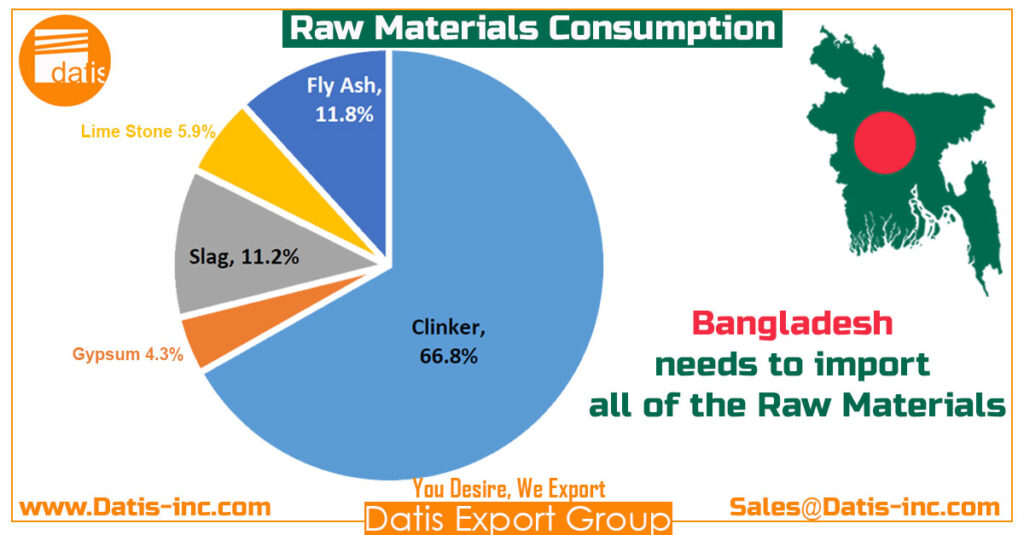

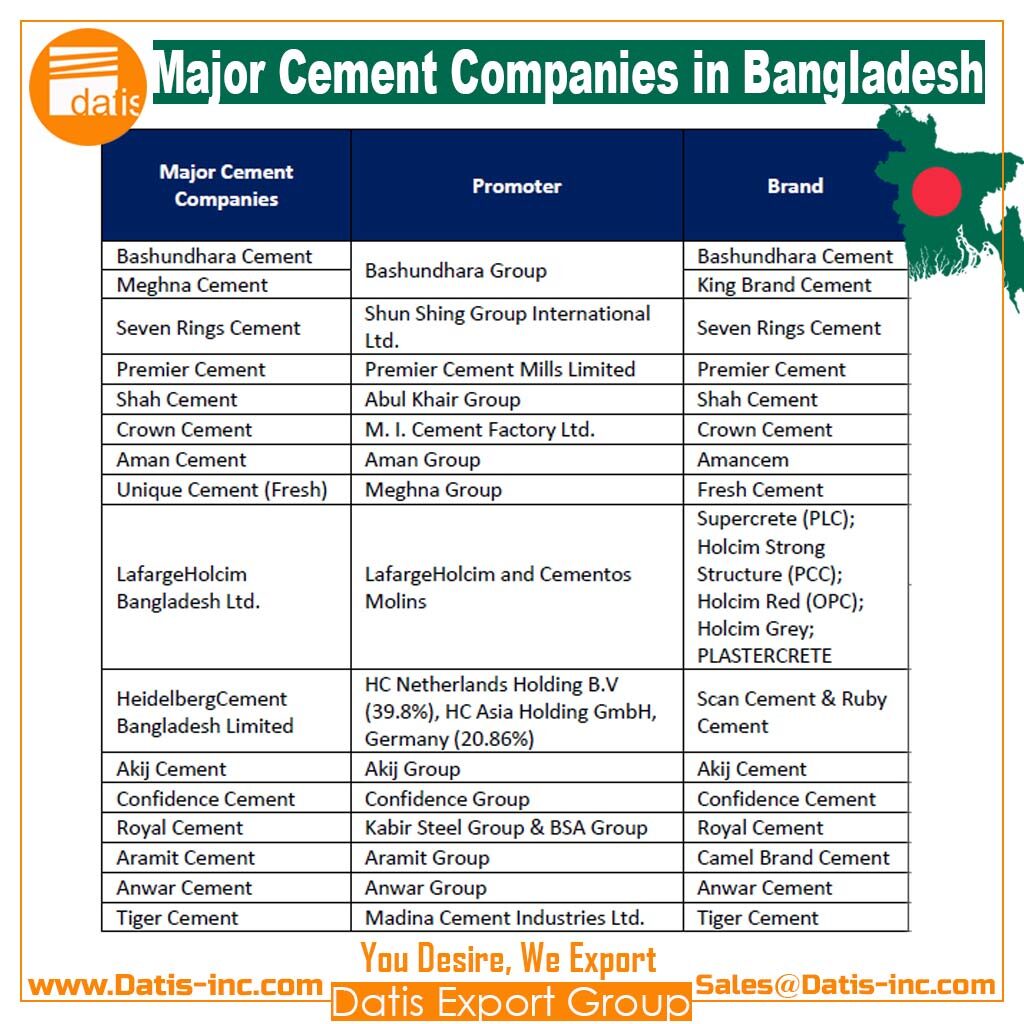

Bangladesh depends on imports and it is one of the largest importers of clinkers globally. Of the 32 cement producers that are currently in operation, only two have clinker production facilities in their own plants. One is Chhatak Cement Factory Ltd, a government owned company, with limited production capacity and the other is LafargeHolcim Bangladesh Limited.

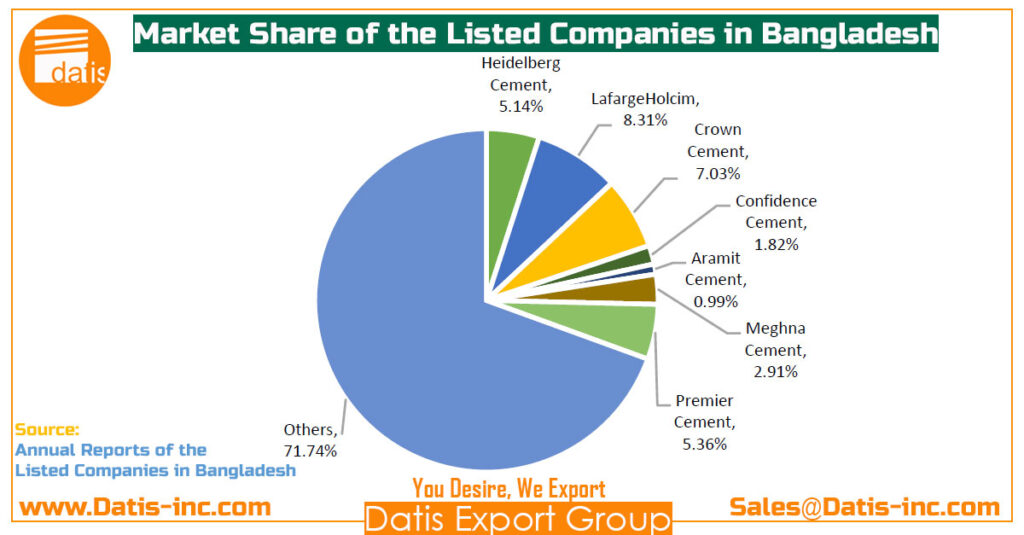

Based on study by EBL securities revealed that Shah Cement holds 14% of the market share, while Lafarge Holcim holds 11.8%, Bashundhara Group, 9.1%, Seven Rings Cement 8.1%, Heidelberg Cement 8%, Premier Cement 6.6%, M.I. Cement (Crown Cement) 6.6%, Fresh Cement 6.5%, Akij Cement 4.2%, and Confidence cement 2%, according to the study.

Shah Cement at a glance:

Shah Cement started on the March 2002. Shah Cement Industries Ltd. is the largest Cement producing plant in Bangladesh, with a capacity of 10 million metric tons per annum.

The plant is situated at Muktarpur, Munshigonj, in the land intersection of two rivers Shitolokkha & Dhaleshwari. It is the largest and one of the most technologically advanced cement plants in Bangladesh. Shah Cement partnered with FLSmidth to commission the world’s most advanced and largest Vertical Mill in Cement Manufacturing. It is the world’s largest single unit mill of its kind.

The world’s largest Vertical Roller Mill at Shah Cement is expected to significantly contribute in improving the quality of housing and play a critical role in the infrastructure development of the country. With its Guinness World Record recognized milestone, Shah Cement is proud to take Bangladesh to a newer height.

Shah Cement Plant is equipped with both inbound & outbound logistic comprising of own ocean going vessels, huge number of cover fleets, barges & bulk carriers to supply in the market place just in time.

Its own bagging plant is one of the largest in this region capable of producing 3 Lac packs per day powered by Hi-tech Star Linger machinery from Austria.

To ensure uninterrupted power supply round the clock, Shah Cement has own power plant of 17-megawatt capacity.

Shah Cement’s commitment to sustainable development, its high ethical standards in business dealings and on-going efforts in community welfare programs have won it acclaim as a responsible corporate citizen.

To provide customer with the best quality concrete, Shah Cement has its own mixing plant, which is equipped with modern PLC-based computer controlled program.

Shah Cement’s efforts in introducing Ready Mixed Concrete coupled with the promotion of bulk cement handling facilities have been responsible for redefining the pace and quality of construction activity in metropolitan cities and in mega infrastructure projects.

The World’s Largest Vertical Roller Mill

has been added in Shah Cement Manufacturing. Guinness World Record has recognized the unique achievement of Shah Cement and has recorded it as the World’s single Largest Cement Vertical Roller Mill facility.

Shah Cement awarded “the best cement brand”

The Leading Cement Brand of the country, Shah Cement was awarded as the ‘Best Cement Brand 2017’ by Bangladesh Brand Forum for the 3rd time which is given based on the joint countrywide survey conducted by Bangladesh Brand Forum and market research agency Kantar Millward Brown.

Shah Cement awarded “Superbrand” in Bangladesh

A concern of Abul Khair Group, the organization received the award for being consistent with their product quality and providing excellent customer service. It was among the 29 brands from diverse industries to have been awarded as the ‘Superbrands’ of Bangladesh for the year 2018-2020.